5 Steps to Financial Freedom

What is financial freedom? It’s different for everyone, but methodologically, financial freedom is when your passive income (from your own business or assets) exceed your expenses... allowing you the freedom to achieve your ideal life... and no longer need to work as an employee!

As you finish your degree and enter the professional workforce possibly for the first time, you’ll soon realise that a degree, reading the Barefoot Investor and a good pay packet won’t be enough to achieve financial freedom. Sure, it’s easy to purchase a flashy car these days, but that decision may not put you on a solid path towards financial freedom.

Imagine being able to afford your dream home, live in your ideal suburb and tick items off your travel bucket list - without having to get out of bed every morning to join the daily grind and make small talk around the water cooler with colleagues about your weekend.

Gianna Thomson, UC alumna and certified financial planner shares with us her 5 simple steps to achieving financial freedom.

5 steps to conquer the financial freedom mountain!

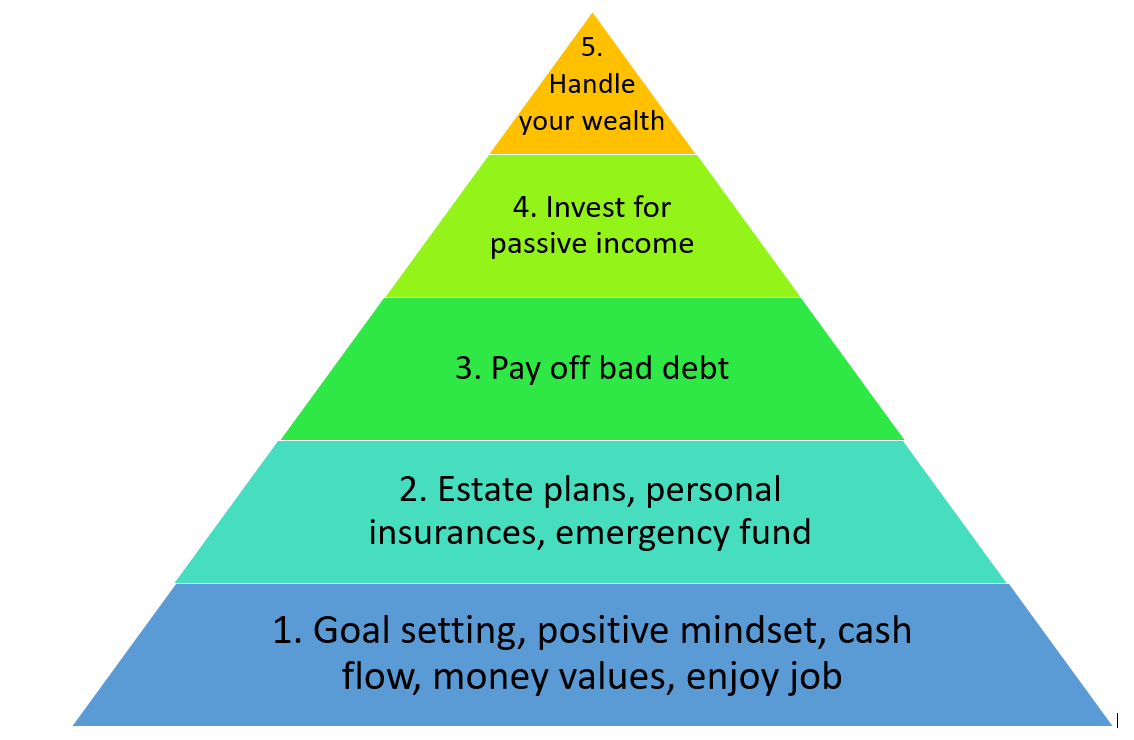

Step 1 – The Foundations

Clarify your goals, motivations and have a positive mindset that you can achieve financial freedom. Have an automatic cash flow and bank account system that includes a budget to identify your discretionary expenses, non-discretionary expenses, and savings plans. Be happy in your job and personal life, as this can help you stay motivated to stick with the plan and reduce rash emotional spending.

Tip: Financial advice can help with your cash flow, money values and goals. A psychologist or accredited life coach can help with your mindset and managing your money blocks.

Step 2 – Plan B

As your journey towards financial freedom is unlikely to always be smooth sailing, create a safety net to protect you and your loved ones in the event of permanent or temporary illness and disability or premature death. Allocate a portion of your cash savings into an emergency fund of approximately 3 months of expenses (depending on your situation such as whether you have a mortgage).

Tip: Personal insurances include income protection, life, total and permanent disability and trauma insurance that considers previous health issues and cash flow affordability. A financial advisor can assist with your risk management strategy and which products are right for you.

![]()

Step 3 – Going, going gone

Pay off consumer debt such as non-tax deductible high-interest credit cards and car loans. There are various strategies to help pay off this debt sooner. A financial adviser or a financial counsellor can advise on the best repayment method for you.

Tip: A financial planner or a financial counsellor can advise on the best repayment method for you.

Step 4 – Invest for passive income

Investing can be done within superannuation or outside superannuation.

Investment asset classes generally include cash, fixed interest, shares, and property, with varying growth and income potential. When devising your investment strategy, some things to consider are investment risk, liquidity, investment timeframe, diversification, preservation rules and tax.

Tip: Seeking investment advice from a professional such as a financial planner is a must do to reduce the risk of inappropriate, costly decisions.

Step 5 – Handle your wealth

Handle your wealth modestly, without overspending or being too generous with your money. Review, monitor and adjunct your investment portfolio when required. Ensure your financial strategy remains up to date as your life and goals change over time.

Tip: An ongoing relationship with a financial advisor can help.

![]()

| Gianna ThomsonBachelor of Finance (2013)Gianna Thomson is a certified financial planner and a Commonwealth superannuation expert, who runs her own financial planning business. You can connect with Gianna through her email - giannathomson@outlook.com.au |